Best Concealed Carry Insurance (2026)

We have compared the price and coverage of the best concealed carry insurance companies on the market. Below we list our top picks and provide you with a break down of each one. We also provide charts comparing their prices and coverages to help you find the plan that works best for you.

We looked at Right To Bear, CCW Safe, USCCA, Attorneys On Retainer, US Law Shield, and Second Call Defense. Find out the results and who we chose for our top pick for concealed carry insurance.

Our Recommended Choice!

We partnered with Right To Bear Association because they provide affordable and comprehensive self-defense coverage designed specifically for responsible gun owners.

SAVE 15% with Code: CCS15

- Most Affordable

- Unlimited Criminal and Civil Defense Coverage

- Add Ons to Customize Your Plan

- Bail Bond Protection costs $4 more per month

Use our discount code CCS15 to save 15% while it lasts!

However, if you are not yet sure which company you want to go with, read on. We will break down each company’s cost and main coverages as well as give a brief overview of each one and what they offer.

Read Concealed Carry Insurance Explained

Best Concealed Carry Insurance Companies

1. Right To Bear

Our Recommended Choice!

Save 15% at Right To Bear with code: CCS15

Pros

Cons

Right To Bear has quickly gained popularity for its strong combination of low cost and comprehensive coverage. It’s a great starting point for those looking to maximize value without sacrificing protection. The program is backed by an “A”-rated insurance carrier, providing added confidence that coverage will be there when it matters most.

One of its biggest advantages is its simple, streamlined structure. Right To Bear offers a single affordable base plan with solid core coverage, then allows you to customize it with optional add-ons. This à la carte approach lets you tailor your protection to your specific needs, so you’re only paying for the coverage you actually want.

If you would like a more in-depth look into Right To Bear be sure to read our Right To Bear Insurance Review where we dig deeper into who they are and what they offer. We are pretty sure you will not find this good of package at a better price.

Important Details

Right to Bear offers a streamlined membership with self‑defense liability coverage purchased on behalf of its members, including criminal and civil defense, bail bonds, firearm replacement, and psychological support for covered self‑defense incidents.

- Price – Individual Membership: $19/month — $205/year (current “Individual Membership” pricing).

- Other Memberships:

- Family Protection Bundle: $40/month — $425/year (two adults plus all children under 18 in the home).

- Law Enforcement & Security Membership: $220/year (for law enforcement, security, and veterans).

- Criminal Defense Coverage: Criminal defense coverage via a self‑defense liability policy obtained for members; protection applies to criminal defense after a covered act of self‑defense.

- Civil Defense Coverage: The same policy provides civil defense coverage for lawsuits arising from a covered self‑defense incident.

- Bail Coverage: Optional add-on; current add-on pricing is $4/month or $35/year, with benefits up to $100,000 for bail-bond expenditures.

- Red Flag Law Coverage: Includes legal defense for Extreme Risk Protection Orders (ERPOs), helping cover legal costs if your firearm rights are challenged through a red flag proceeding

- Choose Your Attorney: Members get 24/7/365 attorney access and legal protection. You can work with counsel under the program’s billing and approval framework, but the exact process follows Right to Bear’s policy and guidelines.

Head over to Right To Bear Insurance to learn more:

2. CCW Safe

Pros

Cons

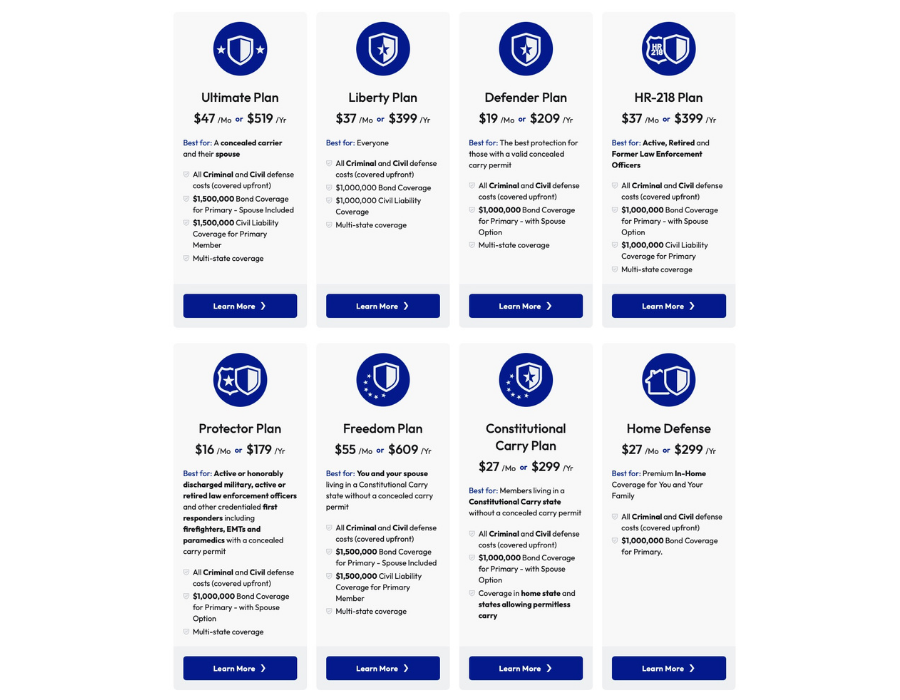

CCW Safe offers a wide variety of concealed carry insurance packages. Each package is geared to fit different customers needs. Some of their packages do have stipulations as to who qualifies or what they will cover.

Some packages require you to have a concealed carry permit, some require you to be active or retired law enforcement, and some are made for specific purposes like Constitutional Carry State, Home Defense or Church Security Plan.

CCW Safe has been in the business for a while and they know what they are doing. Their large selection of specialized plans can help you tailor your coverage to suite your specific needs.

Important Details

CCW Safe is a legal service membership that provides unlimited criminal and civil defense coverage for members involved in covered self‑defense incidents. They offer several plans tailored to different types of carriers.

Key plans relevant to concealed carriers:

- Defender Plan – core CCW plan for most civilians

- Protector Plan – for active/retired military and law enforcement, and qualifying veterans

- Ultimate Plan – premium CCW plan, often with spouse coverage

- Constitutional Carry Plan – for residents in constitutional carry states

- Home Defense Plan – in‑home self‑defense only

- Additional options: HR‑218, Freedom, and other specialized plans

Representative pricing (individual):

- Defender Plan: $19/month — $209/year

- Protector Plan: $16/month — $179/year

- Ultimate Plan: $47/month — $519/year

- Constitutional Carry Plan: $27/month — $299/year

- Home Defense Plan: $27/month — $299/year

- Higher‑level: “Freedom/Liberty” style plans typically range from about $37–$55/month and $399–$609/year, depending on bail and civil‑liability limits.

Coverage highlights (flagship CCW plans like Defender/Ultimate):

- Criminal Defense Coverage: Unlimited criminal defense with no cap on defense costs, including attorneys, investigators, experts, and trial expenses for covered self‑defense incidents.

- Civil Defense Coverage: Unlimited civil defense with no cap on defense costs for covered civil suits.

- Bail Coverage: Plans may include bond coverage up to $1,000,000 or $1,500,000 depending on tier, but CCW Safe pays the bond company fee up to 10% of that amount.

- Civil Liability (Damages): Selected plans include $1,000,000–$1,500,000 in civil‑liability coverage for damages, separate from defense costs.

- Choose Your Attorney: You may choose your own attorney, but CCW Safe must approve them. They also maintain a network of experienced self‑defense attorneys.

Head over to CCW Safe to learn more:

3. Attorneys On Retainer

Pros

Cons

When it comes to legal protection for concealed carry, Attorneys on Retainer (AOR) stands out because they’re not an insurance company at all. Instead, they’re part of the Attorneys for Freedom Law Firm, offering a direct legal defense service. This means you get immediate access to attorneys for criminal or civil defense without the typical insurance policy caveats.

With AOR, you’re covered from the moment of the incident through trials and appeals, including bail, scene cleanup, and even mental health support. Because they aren’t insurance, they don’t have the same focus on minimizing payouts; their goal is full-throttle defense.

Plus, you keep attorney-client privilege from the get-go, which isn’t always guaranteed with insurance policies. If you want straightforward legal support without insurance complications, AOR might just be the way to go.

Important Details

Attorneys on Retainer (AOR) is a law‑firm membership, not an insurance company. Members pay a flat fee to retain a dedicated criminal defense firm that promises full representation for qualifying self‑defense cases nationwide.

- Price – Self‑Protection Plan (Nationwide, individual): $37/month — $390/year. $100 sign up fee.

- Criminal Defense Coverage: For qualifying self‑defense incidents, AOR covers your criminal defense attorney fees from investigation through trial and certain appeals, without additional hourly charges beyond the membership fee.

- Civil Defense Coverage: AOR also covers civil defense attorney fees for qualifying self‑defense incidents.

- Bail Coverage: Membership includes bail‑related assistance and funding up to the limits set in the Self‑Protection Plan (they handle coordination and work to secure your release).

- Choose Your Attorney: AOR is centered on representation through the Attorneys For Freedom law-firm model, but the firm may also work with the member’s choice of local counsel in other jurisdictions.

AOR also lists additional benefits such as a 24/7 emergency hotline, on‑scene advice, incident support, scene clean‑up, firearm replacement, and counseling allowances in its own membership details.

Head over to AoR to learn more:

4. USCCA

Pros

Cons

USCCA offers a well-rounded package that goes beyond legal protection, combining training, education, and member discounts. Each membership includes the same Self-Defense Liability Insurance, but what really sets USCCA apart is its focus on helping members become more informed and prepared concealed carriers.

One of the standout benefits is access to educational resources and training opportunities. Members can take advantage of a wide range of courses (some may require an additional fee), along with regularly updated content that helps answer common—and not-so-common—concealed carry questions.

A particularly useful tool is their Concealed Carry Reciprocity Map, which allows you to quickly check and stay up to date on firearm laws across different states—an essential resource for anyone who travels while carrying.

Here are a list of just some of the benefits that come with USCCA membership:

TRAINING

- Concealed Carry Magazine subscription

- Self-defense guides and checklists

- Connection to certified firearms instructors

- Expert-led, scenario-based training videos

MEMBER PERKS

- Spouse membership discounts

- Exclusive discounts on USCCA products

- Up to 30% savings from industry partners

- Reliable, around-the-clock service

We used to be partnered with USCCA, but recently we ended that partnership. Due to their large increase in prices, as well as some recent conflicts in the media, we decided to move them slightly down our list.

Important Details

Current Pricing (Individual)

- Gold: $39/month — $399/year

- Platinum: $49/month — $499/year

- Elite: $59/month — $599/year

Core Legal Coverage (All Tiers)

- Criminal Defense / Attorney Fees: Up to $250,000 for covered self-defense incidents

- Civil Defense and Damages: Up to $2,000,000 per occurrence (self-defense liability policy limit)

- Bail Coverage: Up to $250,000 for bail bond funding and related legal expenses

- Choose Your Attorney: Yes — you may select your own attorney, subject to approval and policy guidelines

- Upfront Payments: Legal costs are paid upfront for covered claims, not reimbursed later

Head over to USCCA to learn more:

5. US Law Shield

Pros

Cons

US Law shield is a company that has been around quite a while and has a good track record in the industry. They offer similar coverage that the other companies on the list offer and a low price. The only downfall is that they get to choose your attorney. If you want to choose your own you may want to look elsewhere.

We heavily value the ability to choose your own attorney. This was a big sticking point with us, and it kept US Law Shield from moving any further up our list. However, they do offer decent coverage and a good price.

You may see this listed as Texas Law Shield sometimes. That is due to the company starting out under that name and then expanding their coverage to the rest of the country and becoming US Law Shield.

Important Details

U.S. LawShield is a legal defense membership focused on providing unlimited attorney coverage for members involved in covered self-defense incidents. Pricing and available options can vary by state and are selected during the sign-up process.

- Price – Base Coverage (Individual): Membership starts at approximately $10.95 per month; final pricing depends on your state and any add-ons you choose

- Criminal Defense Coverage: Unlimited attorney fees for covered criminal self-defense cases, with no caps, hourly limits, or deductibles

- Civil Defense Coverage: Unlimited attorney fees for covered civil defense cases

- Bail Coverage: Available as an optional add-on; coverage amounts and pricing vary by state and are shown during sign-up

- Choose Your Attorney: No — members are represented through U.S. LawShield’s network of independent program attorneys.

Because pricing is state‑specific, it’s best in your article to say that membership “starts at $10.95/month” and note that final cost is determined by state and add‑ons at checkout.

Head over to US Law Shield to learn more:

6. Second Call Defense

Pros

Cons

Second Call Defense is a membership-based program that provides legal and financial protection for individuals involved in covered self-defense incidents. Their services include immediate access to an attorney, upfront funding for legal defense, bail bond assistance, and civil defense coverage.

The goal is to remove the financial burden after a defensive incident, allowing you to focus on your safety, recovery, and next steps.

Important Details

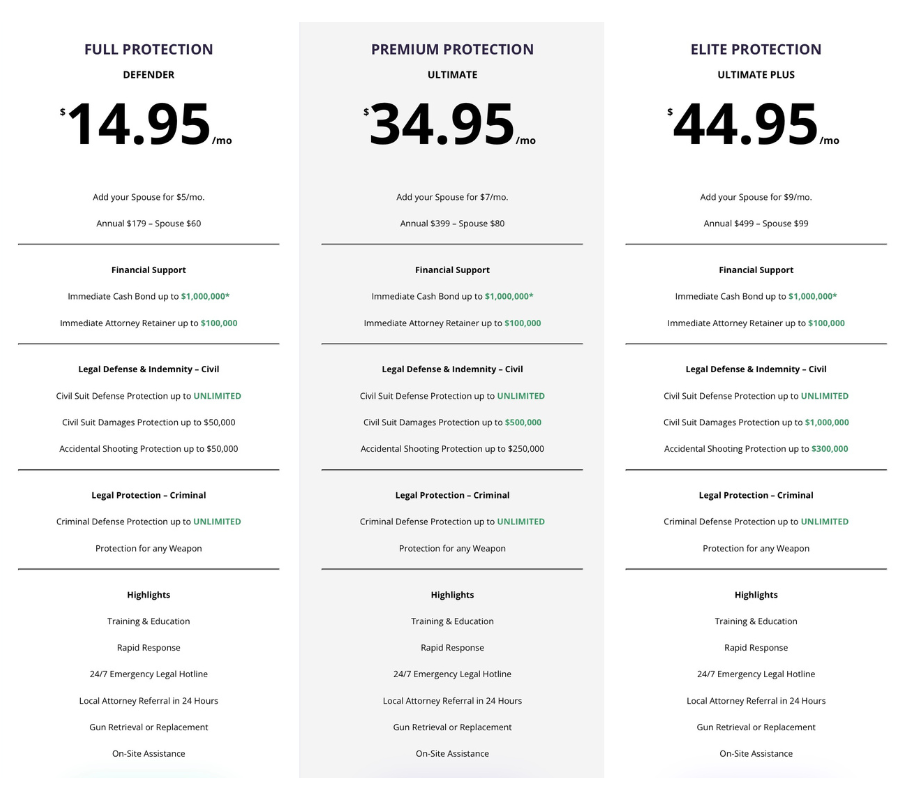

Second Call Defense uses a tiered membership structure, offering increasing levels of protection as you move up in plans.

Key Plans (Individual)

- Basic Plan – entry-level option with limited benefits

- Full Protection – Defender Plan – most popular core protection tier

- Higher tiers – Ultimate and Ultimate Plus for expanded coverage

Representative Pricing (Individual)

- Basic: $9.95/month — $119/year

- Full Protection – Defender: $14.95/month — $179/year

- Ultimate: $34.95/month — $399/year

- Ultimate Plus: $44.95/month — $499/year

- Spouse Add-On: ~$5/month on Defender (higher tiers ~$7–$9/month depending on plan)

Coverage (Defender and Above)

- Criminal Defense Coverage: Unlimited criminal defense for covered self-defense incidents

- Civil Defense Coverage: Unlimited civil defense coverage on Defender, Ultimate, and Ultimate Plus plans

- Bail Coverage: Up to $1,000,000 in bail bond coverage depending on plan

- Civil Damages: Tier-based coverage — $50,000 (Defender), $500,000 (Ultimate), up to $1,000,000 (Ultimate Plus)

- Choose Your Attorney: Members have access to a nationwide network of vetted attorneys and immediate legal support following an incident

Head over to Second Call Defense to learn more:

Concealed Carry Insurance Companies Compared

Below, you’ll find simple charts that break down the prices and coverages of the concealed carry insurance companies we listed above. These comparisons make it easier to see what each provider offers so you can choose the one that fits your needs best. If you’re looking to protect yourself or reevaluating your current plan, this info will help you make a confident decision.

Concealed Carry Insurance Price Compared

The chart below breaks down the pricing for top concealed carry insurance providers, making it easy to compare your options.

| Insurance Program | Base Plan (Individual) | Monthly Cost | Yearly Cost |

|---|---|---|---|

| Right To Bear | Individual Membership | $19 | $205 |

| CCW Safe | Defender Plan | $19 | $209 |

| *Attorneys On Retainer | Self-Protection Plan | $37 | $390 |

| USCCA | Gold Membership | $39 | $399 |

| *U.S. LawShield | Base Coverage | $11 | $132 |

| Second Call Defense | Full Protection – Defender | $15 | $179 |

Note: Attorneys on Retainer typically requires a one-time $100 setup fee.

Note: U.S. LawShield pricing varies by state, and final costs depend on your location and selected add-ons.

Concealed Carry Insurance Coverage Compared

The following chart compares the coverage options from different concealed carry insurance companies, helping you find the best fit for your needs.

| Category | Right To Bear | CCW Safe | Attorneys on Retainer | USCCA | U.S. LawShield | Second Call Defense |

|---|---|---|---|---|---|---|

| Model Type | Insurance | Membership | Law Firm | Insurance | Law Firm | Insurance |

| Criminal Defense | Unlimited | Unlimited | Unlimited | Up to policy limits | Unlimited | Unlimited |

| Civil Defense | Unlimited | Unlimited | Unlimited | Up to policy limits | Unlimited | Unlimited |

| Civil Damages | None | $1M–$1.5M (select plans) | $100,000 | $2,000,000 | None | $50k–$1M (plan-based) |

| Bail Coverage | +$4/mo add-on (up to $100k) | Up to $1M–$1.5M bond (10% covered) | Plan-based assistance | Up to $250k | +$2.95/mo add-on | Up to $1M (plan-based) |

| Psych Support | Yes | Up to 40 sessions | Yes (limited) | No | No | Yes |

| Choose Attorney | Yes | Approved | Firm-led (may coordinate local counsel) | Approved | No (network only) | Network-based with coordination |

| Red Flag Laws | Yes | Optional add-on | Up to $15,000 | Included | Included | No |

| Overall Value | ⭐Best Overall | ⭐Strong Alternative | Niche Option | Higher Cost | Budget Option | Mid-Tier Option |

How We Compared Concealed Carry Insurance Companies

We’ve carefully compared the top concealed carry insurance companies based on two key factors: coverage and price. The sections below break down these aspects to give you a clear view of how each provider stacks up.

Coverage

We looked at key areas like Criminal Defense, Civil Defense, and additional benefits each provider offers. These factors are crucial in ensuring you have the right protection if you ever need it.

Criminal Defense Coverage

Criminal Defense coverage helps protect you if you’re involved in a self-defense incident that results in criminal charges. This coverage ensures you have access to legal representation and can help cover the costs of your defense.

Unlimited or high-limit criminal defense coverage is important because legal fees can quickly add up, especially in complex cases. With unlimited coverage, you won’t have to worry about running out of resources to fight for your rights and defend yourself in court.

Civil Defense Coverage

Civil Defense coverage comes into play if you’re sued after using your firearm in self-defense. It covers the costs associated with defending yourself in a civil court, where the focus is on whether you’re liable for damages, rather than criminal guilt.

Having solid Civil Defense coverage is crucial, as lawsuits can be expensive and time-consuming. This protection helps ensure you’re not left financially exposed if someone decides to take legal action against you after an incident.

Other Coverages

Under “Other Coverages,” we’ve considered a range of additional protections that can make a big difference in a stressful situation. These include:

- Bail Bond Coverage: Helps cover the cost of your bail if you’re arrested after a self-defense incident. This ensures you can get out of jail while you await trial or further proceedings.

- Choice of Attorney: Some providers allow you to choose your own attorney, giving you more control over your defense and ensuring you have the right legal expertise for your case.

- Firearm Replacement: If your firearm is confiscated or damaged during a self-defense incident, this coverage can help cover the cost of replacing it.

- Expert Witness Coverage: In many self-defense cases, expert witnesses are crucial to establishing the validity of your actions. This coverage helps pay for expert testimony, which can make a significant difference in court.

- Psychological Support: After a traumatic incident, psychological support can be essential for your well-being. This coverage helps you access counseling or therapy to cope with the emotional aftermath.

- 24-Hour Hotline: Many providers offer access to a 24-hour legal and emergency hotline, so you can get immediate advice and assistance in the crucial moments after a self-defense incident. This ensures you’re not left to navigate the situation alone, no matter the time of day.

These additional coverages help ensure you’re fully protected throughout the legal and personal challenges that may follow a self-defense situation.

Price

Price is a major factor for many when choosing concealed carry insurance, as it needs to fit within your budget while still offering the protection you need.

We’ve compared the monthly costs for each provider, as well as the potential savings you can get by opting for a yearly plan. A yearly plan often provides a more affordable option in the long run.

In addition, we also took a close look at any add-ons or optional coverages that can be included with your policy, which can impact the overall cost. Discounts were another key area we considered, if you get a decent discount off the yearly payment, it can make a huge difference.

Conclusion

Our Recommended Choice!

Right To Bear Insurance stands out among competitors for its strong balance of comprehensive coverage and affordability, offering unlimited criminal and civil defense at a budget-friendly price.

We partnered with Right To Bear Association because they provide affordable and comprehensive self-defense coverage designed specifically for responsible gun owners.

SAVE 15% with Code: CCS15

- Most Affordable

- Unlimited Criminal and Civil Defense Coverage

- Add Ons to Customize Your Plan

- Bail Bond Protection costs $4 more per month

Save 15% at Right To Bear with code: CCS15

It provides excellent value for concealed carry holders seeking reliable legal protection. Their upfront payment model—rather than reimbursement—helps remove the immediate financial burden following a self-defense incident, which can be critical in high-stress situations.

In addition, Right To Bear allows you to customize your plan with optional add-ons, so you only pay for the coverage you actually need. Altogether, this combination of flexibility, value, and solid protection makes Right To Bear a top choice for those looking for both peace of mind and cost-effective coverage.

If you’re considering an alternative, CCW Safe is another excellent option. It offers unlimited legal defense coverage along with a strong reputation for member support, all at a competitive price point.

CCW Safe is great for concealed carry license holders, law enforcement, and military. They have also recently added a plan that covers people without licenses in constitutional carry states.

Just be sure that you are eligible for the package you choose.

- Upfront Unlimited Legal Defense Costs

- Large Variety of Coverage Options

- High Bond and Liability Limits

- For Cheapest Plan You Must Have CCW License

Ultimately, the right concealed carry insurance comes down to your individual needs and priorities. Both Right To Bear and CCW Safe provide high-quality protection and are strong choices for anyone looking for added peace of mind.

If you want to learn more about getting started, be sure to check out our 5 Step Guide to Concealed Carry.